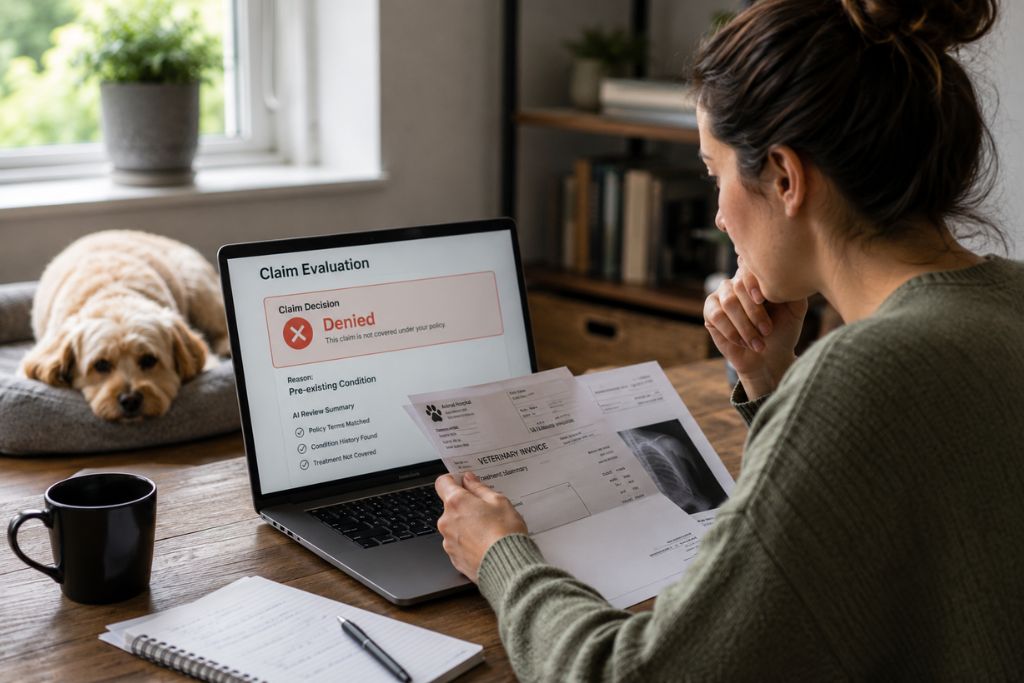

What makes these denials especially risky is that many policyholders believed they had protection in place for their pets, only to learn after diagnosis that the insurer considers the condition excluded.

Florida legislation does not allow automatic exclusions without clear disclosure, and not every genetic-based denial meets those standards. Understanding how these companies apply congenital and hereditary exclusions is more than necessary before accepting a denial as final.

We’ll explain how these exclusions work under current state law and when they can be challenged. Let’s dive right in.

What are Congenital Conditions in Pet Insurance?

Congenital conditions are present at birth, even if they are not immediately detectable, while hereditary conditions are linked to genetic inheritance and may develop later in life.

The company managing the policy frequently blurs this distinction when issuing a congenital hereditary pet insurance denial. Also, these definitions matter because exclusions must be precise, always:

- How congenital conditions are identified and documented.

- Whether hereditary conditions must be clinically diagnosed.

- If and when symptoms trigger an exclusion.

- How policyholders are informed of these limitations.

A congenital or hereditary condition exclusion must have a clear identification, documented diagnosis, and transparent communication. They are very needed to determine whether an exclusion is enforceable or open to challenge.

Common Ways Insurers Deny Claims Based on Genetics

Insurers rely on predictable patterns when denying claims related to genetic factors. These patterns include:

- Orthopedic issues such as hip dysplasia as hereditary without addressing when symptoms first appeared.

- Cardiac conditions as congenital despite a lack of symptoms at enrollment.

- Neurological diagnoses to retroactively apply a congenital condition exclusion.

- Multiple conditions under a single genetic label to avoid claim-by-claim evaluation.

In many cases, they rely on generalized breed-based assumptions rather than the actual and specific insured pet’s medical history.

Florida standards do not allow exclusions to be applied solely based on predisposition or statistical likelihood, so each claim must be evaluated using documented medical evidence and the specific terms of the policy.

Predisposition vs. Diagnosed Condition: Why It Matters

A predisposition indicates an increased likelihood of developing a condition; it does not confirm the presence of disease. Despite this distinction, predisposition is often mistakenly treated as grounds for exclusion. This distinction is critical because:

- A genetic marker alone does not constitute a medical condition.

- Florida law requires exclusions to be tied to diagnosable conditions.

- Coverage decisions must rely on clinical findings, not probabilities.

Here, insurers tend to fail explaining how or when the condition became active.

This approach places the burden unfairly onto the policyholder, where proper evaluation requires veterinary confirmation, documented onset, and a clear connection to the exclusion language in the policy.

Florida Law and the Burden of Proof on Insurers

Under Florida Statutes Section 627.71545, policy issuers must clearly disclose exclusions and demonstrate that they apply to the specific claim at issue. This standard is reinforced by guidance from the National Association of Insurance Commissioners through the Pet Insurance Model Act, so they must be able to show:

- Exclusion was clearly disclosed at the time of purchase.

- Condition meets the policy’s definition of congenital or hereditary.

- Diagnosis occurred under circumstances triggering the exclusion.

- Denial aligns with how similar claims are handled.

If any part of that chain is missing, the denial may lack legal foundation and become subject to challenge, particularly when coverage decisions contradict the policy language or prior claim handling practices.

All of this is reinforced by regulatory frameworks supported by organizations such as NAIC, which establishes standards focused on disclosure and fair claims handling. These principles are reflected in Florida’s regulatory approach, including the application of HB 655 law to pet insurance coverage and exclusion practices.

How a Pet Insurance Attorney Can Challenge These Denials

A pet insurance attorney in Florida focuses on aligning medical evidence with policy language and Florida disclosure standards to determine whether the insurer’s position is enforceable:

- Analyzing the policy to determine how congenital and hereditary exclusions are defined.

- Comparing veterinary records against the insurer’s stated basis for denial.

- Identifying reliance on predisposition rather than diagnosed condition.

- Evaluating whether the insurer met its burden of proof.

- Challenging inconsistent or selective application of exclusions.

Working in coordination with broader Florida insurance dispute experience through firms such as The Gross Group, these cases are approached using established coverage principles adapted to pet insurance claims.

If your pet’s claim was denied based on a genetic or congenital condition, requesting a professional claim review to The Gross Group, Your Pet Attorneys can clarify whether the insurer’s decision complies with Florida law or should be formally challenged.

Frequently Asked Questions (FAQs)

1. Can pet insurance deny claims for congenital conditions?

Not automatically. Insurers must clearly disclose the exclusion and prove it applies to the diagnosed condition.

2. Is a genetic predisposition the same as a diagnosed condition?

No. A predisposition alone does not justify denying coverage under Florida standards.

3. What conditions are commonly denied as genetic?

Orthopedic, cardiac, and neurological conditions are frequently cited, but each requires individual evaluation.

4. Who has the burden of proof in genetic exclusions?

The insurer must prove that the exclusion applies and was properly disclosed.

5. How can I dispute a denial based on a genetic condition?

A pet insurance attorney can assess the policy, medical records, and denial for legal compliance.