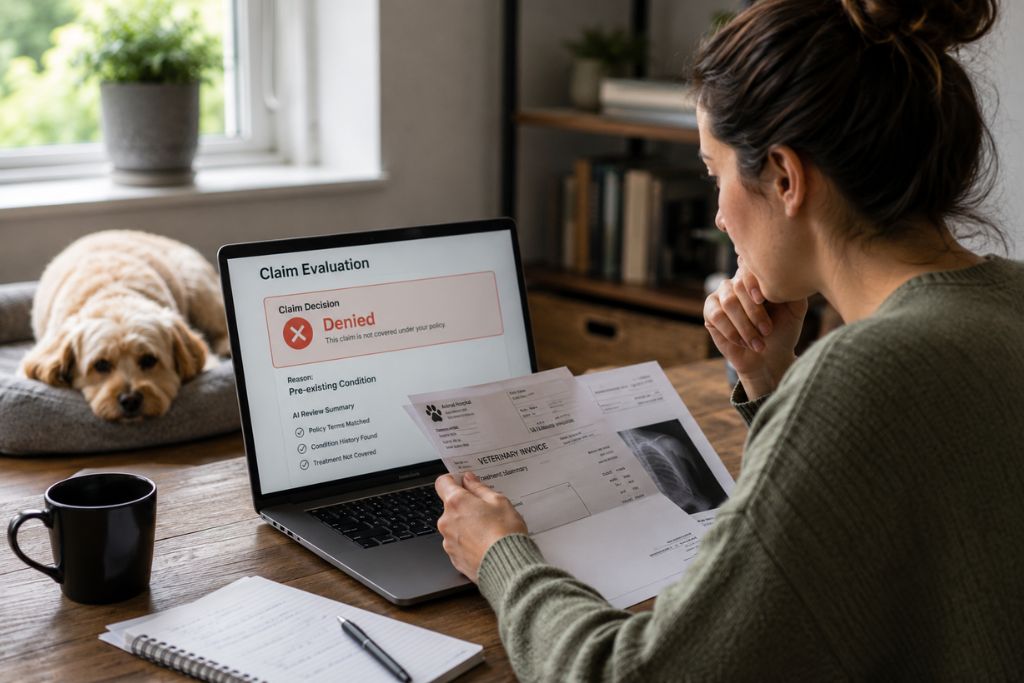

Artificial intelligence is becoming a standard part of how coverage companies process and review pet health claims. Automated systems now play a role in the outcome of many claim evaluations, sometimes before a human adjuster even opens the file.

Understanding how these systems work, and where they fall short, helps you navigate the process with realistic expectations and know when to push back. Let’s begin.

How pet insurance claims are evaluated today

Traditionally, this process relied almost entirely on human reviewers who could exercise judgment when a case was ambiguous or when a vet’s notes required medical interpretation.

That approach took time, but it allowed for nuance; a reviewer could flag an unusual case, request additional records, or escalate a decision when the situation didn’t fit neatly into the policy’s definitions.

Today, many policy issuers have introduced automated tools to handle the initial stages of this review. Processing pet insurance claims through software speeds up intake, reduces manual data entry, and allows companies to handle higher volumes with leaner teams; but it also means early decisions are increasingly made without direct human oversight.

The role of Artificial intelligence in modern claim evaluations

For pet insurance in Florida, where the number of insured pets has grown steadily alongside the state’s population, AI helps insurers keep pace with demand. Automated systems can also apply the same initial criteria across every claim without variation based on reviewer experience or workload.

Still, AI in this context is best understood as a tool that assists and influences the process, not one that replaces professional judgment.

5 risks to consider when pet insurance claim evaluations involve AI

1. Limited medical context

When your pet’s claim involves a condition with overlapping symptoms, or a treatment that sits at the boundary between preventive and corrective care, an automated system may categorize it based on surface-level data alone.

2. Overreliance on historical patterns

Embrace and companies with similar evaluation models are increasingly using pattern recognition to assess claims; but if those patterns were built on incomplete or inconsistent past decisions, new claims may be evaluated against a flawed baseline.

3. Faster decisions with less review depth

Healthy Paws and other animal insurance providers openly promote rapid claim processing as a feature, and in straightforward cases it genuinely is one; but a quick turnaround on a complex claim can be a sign that key details weren’t examined closely.

4. Broad interpretation of policy terms

Automated systems tend to apply definitions literally and consistently, which can work against policyholders when the wording is broad or when a term like “chronic condition” covers more ground than expected.

If the system reads your policy’s exclusion list in the most restrictive way possible, it may deny coverage for something a human reviewer would have approved.

5. Data gaps or incomplete records

Figo and similar policy issuers encourage policyholders to submit thorough documentation precisely because missing or inconsistent records can trigger automatic denials, even when the underlying treatment clearly qualifies under the policy.

Pet insurance companies using technology in claim evaluations

Several of the leading pet insurance companies in Florida increasingly rely on automated systems as part of their claims process.

Below is a brief overview of companies that incorporate advanced technologies into their evaluation process:

- Lemonade uses an AI model called AI Jim to review and process pet claims; some straightforward cases are resolved in seconds through fully automated review.

- Trupanion offers direct vet pay and same-day claim processing at participating clinics, relying on automated verification to support real-time decisions.

- Nationwide processes claims through an online portal and may use AI-assisted tools to match submitted documentation against policy coverage terms.

- ASPCA incorporates automated intake systems to screen claims before they reach a human adjuster.

- Spot Pet Insurance provides a digital submission platform that likely incorporates automated review at the intake stage, based on its published turnaround commitments.

- Fetch Pet Insurance promotes fast digital claim handling, which in practice reflects some degree of automation in the early stages of evaluation.

- Pets Best highlights quick reimbursement timelines as a core feature, and rapid processing at scale typically relies on automated systems to handle initial review.

How Florida law applies to claim evaluations

Florida insurance law places specific obligations on coverage companies, regardless of how they process claims internally. Under the state’s bad faith statute, insurers are required to conduct a reasonable investigation, communicating clearly with policyholders, and not delaying or denying valid claims without grounds.

The Florida Unfair Insurance Trade Practices Act also prohibits certain conduct in claims handling, including misrepresentation of policy terms, arbitrary denials, and unreasonable delays.

The Florida Pet Insurance Act (HB 655) established clearer disclosure and regulation requirements for pet coverage sold in the state, reinforcing the expectation that policy terms be applied fairly and consistently.

Florida insurance attorneys who specialize in coverage disputes can help you assess whether an AI-assisted denial crosses the line from a legitimate coverage decision into a practice the law prohibits.

Why legal guidance matters in AI-supported evaluations

When an automated system denies or underpays a claim, the reasoning it provides is often a code, a brief explanation, or a reference to a policy exclusion. It rarely offers transparency about how the decision was made, which records were considered, or whether the algorithm applied your policy’s terms correctly.

Your Pet Attorneys works with policyholders across Florida to:

- Review denied or underpaid claims and identify whether the evaluation result is consistent with your actual coverage.

- Analyze policy language in detail, including exclusions, definitions, and any ambiguous terms the automated system may have interpreted against you.

- Document the decision trail, pulling together veterinary records, correspondence, and claim history to build a complete picture of what happened.

- Challenge decisions that don’t hold up, whether through a formal appeal with your insurer or through legal channels when good faith obligations have not been met.

If a decision you received doesn’t match what your policy actually promises, it’s worth having someone review the documentation before you accept it as final. You can talk to a pet insurance attorney to get an assessment of your situation without any obligation.

When technology influences the outcome

AI is a powerful tool, but it isn’t a final authority.

The law in Florida gives you the right to contest a decision you believe was handled incorrectly, regardless of how it was generated. If your claim was denied or came back at a lower amount than expected, the reason may have more to do with how a system categorized your documents than with what your policy actually covers.

Knowing that difference exists, and knowing that you have options, can change the outcome.