Caring for a pet brings daily joy, companionship, and a sense of responsibility that many owners deeply value. Alongside that bond comes a growing commitment: pet costs have been steadily increasing, shaped by better veterinary care, new treatments, and higher standards of well-being.

For many households, these expenses are now a meaningful part of the monthly budget. But this isn’t a negative trend, it reflects how much more we can do today to protect and care for our pets. Planning ahead simply becomes part of being a responsible pet owner.

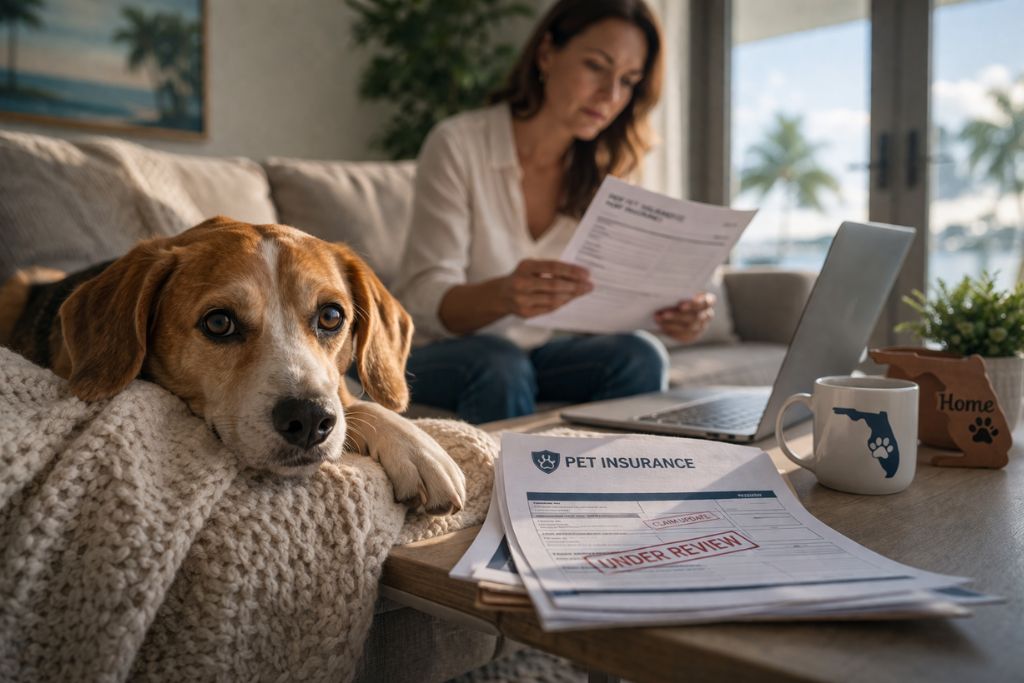

Pet insurance is one of the tools many families use to manage these rising pet costs. Still, it’s important to understand that it doesn’t cover everything. Knowing how costs, coverage, and limitations work together can help you make smarter decisions for your pet’s long-term care.

Understanding Pet Costs Today

Pet costs have been rising steadily, driven by advances in veterinary care, inflation, and higher standards of treatment. According to the American Pet Products Association, U.S. pet owners spend over $100 billion annually, with average yearly costs for dogs and cats typically ranging between $1,000 and $2,500 when food, routine veterinary visits, and preventive care are included.

Over time, these expenses can add up significantly. For example, maintaining a pet over 10–15 years may represent tens of thousands of dollars in total care. In cases involving chronic conditions or emergencies, annual veterinary expenses alone can reach several thousand dollars, based on data from the American Veterinary Medical Association.

Everyday pet costs include food, vaccines, parasite prevention, and wellness exams, while surgeries or specialist care add unpredictable expenses. These figures illustrate how average costs work in practice, and why planning ahead is essential.

Why Pet Costs Are Rising?

The price of pet services including veterinary care, grooming, and boarding, rose 38% from January 2021 to January 2026, according to data from the Department of Labor. Veterinary care alone increased even faster, climbing about 43% over the same period.

Part of what’s driving that increase is that pets now have access to advanced diagnostics, oncology services, orthopedic surgery, dental care, and programs that simply didn’t exist in most practices a generation ago.

Recent data found that revenue was up slightly for veterinary services, but visits were down, suggesting that most visits are costing more while people are going to the vet less frequently.

How Pet Owners Are Planning for These Costs

When asked how they’d handle a large vet bill they couldn’t cover immediately, owners cite a mix of: personal savings, credit cards, payment plans offered by clinics, and in some cases crowdfunding. About 15% report setting aside money in a dedicated pet savings account.

Pet insurance has become one of the most widely adopted tools for managing rising animal care expenses, as the U.S. saw a 12.7% increase in total insured pets in 2024 compared to 2023, and premium volume has more than doubled since 2020.

The goal is to reduce the financial shock when something goes wrong, so that the decision you face is medical, not monetary. Also, understanding how pet coverage claims typically unfold gives you a clearer picture of the need for coverage at all times.

What Pet Insurance Covers? and What It May Not

| Category | Typically Covered | Typically Not Covered |

|---|---|---|

| Accidents and Illnesses | Emergency treatment, surgery, hospitalization, diagnostic tests, prescription medications | - |

| Chronic & Hereditary Conditions | Diabetes, arthritis, breed-related conditions (depending on plan) | Conditions classified as pre-existing |

| Specialist & Advanced Care | Specialist visits, imaging (X-rays, ultrasounds), sometimes alternative therapies | Treatments linked to excluded or pre-existing conditions |

| Waiting Periods | Coverage applies after the waiting period ends | Claims for conditions that appear during the waiting period |

| Preventive & Routine Care | May be included as an add-on (wellness rider) | Routine exams, vaccines, dental cleanings (in standard plans) |

| Breed-Specific Conditions | May be covered depending on policy terms | Conditions excluded due to breed predisposition |

When Insurance Doesn’t Cover the Full Pet Cost

A partial reimbursement might happen because the policy issuer determined that part of the treatment related to a pre-existing condition, or because the procedure was coded in a way that fell outside the covered category.

Knowing this can help you build a more complete financial plan, and prepare you to respond effectively when a claim doesn’t go the way you expected.

What You Can Do If Your Coverage Falls Short

- The explanation of benefits your coverage sends should reference specific policy language; find that language in your original documents and read it carefully

- You’re entitled to a clear, specific reason, not just a claim code or a generic reference to exclusions

- Gather all veterinary records, invoices, the full treatment history for the condition in question, and any prior communications with the insurer

- Ask your vet to provide a letter of medical necessity if the treatment was discretionary or if the condition classification is in dispute

- File a formal written appeal, with all supporting documents attached, and send it with a record of delivery

- Track every date, representative names, reference numbers

- Research whether your state has a Department of Insurance complaint process (Filing a complaint is a formal step, but it’s an available one)

When Professional Guidance Can Help

Florida insurance lawyers are the most useful: when a claim involves a significant dollar amount and the denial seems inconsistent with what the policy says; when the company has changed its position multiple times or been slow to respond; or when the exclusion being cited involves ambiguous language that a reasonable person could interpret more than one way.

Pet insurance is a regulated product, that’s a fact, and policy issuers are required to honor the terms of the contracts they sell.

When there’s a genuine question about whether a denial falls within those terms, legal review can clarify what you’re owed, and in some cases, help you recover it.

Planning Ahead: Protecting Your Pet and Your Finances

- Read the exclusions section of any policy before you buy it: it’s the part that defines what the policy actually covers.

- Choose your coverage based on your pet’s specific risk profile (breed, age, known conditions). A lower-cost plan with more exclusions can end up costing more in the long run.

- Set a dedicated savings buffer for co-pays, deductibles, excluded conditions, and the waiting periods before coverage activates

- Revisit your coverage terms, your pet’s health status, and your financial situation annually

A Florida pet lawyer can also help you review existing coverage for potential issues before they become disputes.

Your Pet’s Health Deserves a Solid Plan

If you’re dealing with a denied or underpaid claim, request a free legal review today. We can help you understand your options.