A single emergency vet visit can run anywhere from $1,500 to over $5,000, and that’s before surgery, hospital stays, or specialist fees. For most pet owners, this lands without warning, right when there’s no financial cushion to absorb it.

The idea behind pet insurance is pretty simple: spread the risk, pay a manageable monthly premium, and let the policy handle the heavy lifting when something goes wrong. But, it depends on factors like your pet’s age, breed, medical background, and, frankly, on how your policy issuer handles claims. Let’s break it down.

Three scenarios tend to define whether pet coverage is a smart move or a very expensive habit. Let’s begin.

Scenario 1: A Young and Healthy Pet

A healthy two-year-old with no history of illness is statistically unlikely to rack up major veterinary costs in the near term and most visits stay routine: vaccines, annual checkups, maybe the occasional minor injury.

Some pet owners find that building a savings fund is a more flexible approach. Others prefer the certainty of a policy, especially knowing that vet costs in South Florida and other urban areas tend to run higher than the national average.

But, not every pet owner needs coverage from day one. If your pet is young and you have the discipline to set aside $50 to $100 a month into an emergency account, you may be in a reasonable position without a formal policy.

Still, even for healthy young pets, understanding what a policy would cover is worth the time. You can review what pet insurance companies in Florida typically include before deciding whether to self-insure or buy a plan.

Scenario 2: A High-Risk or Aging Pet

A seven-year-old with a history of joint issues, a breed prone to cardiac conditions, or a pet that’s already completed treatment for cancer, all signal that future vet costs are not a matter of if, but when and how much.

This is where animal coverage delivers the most value, provided you enrolled before those conditions were documented. Policy issuers almost universally exclude pre-existing conditions, meaning anything your pet was treated for before the policy’s effective date is off the table.

If you’re enrolling an older pet, expect a more thorough review of their medical history and a higher premium. That premium reflects that older animals file claims more often and at higher dollar amounts.

Also, reviewing pet insurance claims history and complaint records for a policy issuer before signing can save you from an unpleasant surprise.

Scenario 3: An Emergency, and a Denied Claim

The one nobody plans for and everyone fears.

Your pet has a sudden condition requiring immediate surgery, and the vet bill comes to several thousand dollars. You’ve been paying your premium faithfully and filed the claim expecting reimbursement. Then you get the denial letter.

The company argued the condition was pre-existing, that the treatment fell outside the policy’s defined scope, or that the documentation submitted didn’t meet their requirements. You’re now out thousands of dollars and trying to understand why the policy isn’t covering what you assumed it would.

When a denial feels wrong, getting a pet lawyer in Florida involved can make a measurable difference in the outcome.

Why Pet Insurance Claims Get Denied

Coverage companies don’t deny claims arbitrarily as they follow policy language, but that language is often written to give them significant discretion:

- Pre-existing conditions: coverage companies sometimes flag conditions as pre-existing based on vague notes in vet records, even when the actual formal diagnosis came later. It’s one of the most disputed grounds for denial in Florida.

- Waiting periods: most policies include a 14- to 30-day window after enrollment during which illness claims aren’t covered.

- Policy exclusions: routine and preventive care, elective procedures, cosmetic treatments, and certain hereditary conditions commonly appear on that listplan, and the exclusions aren’t always easy to locate in the policy document.

- Underpayment: fixed payout tables that don’t align with what vets in your area actually charge.

- Incomplete documentation: documentation standard is higher than most people expect going in, and a single missing record can derail an otherwise valid claim.

What to Do If Your Pet Insurance Claim Is Denied

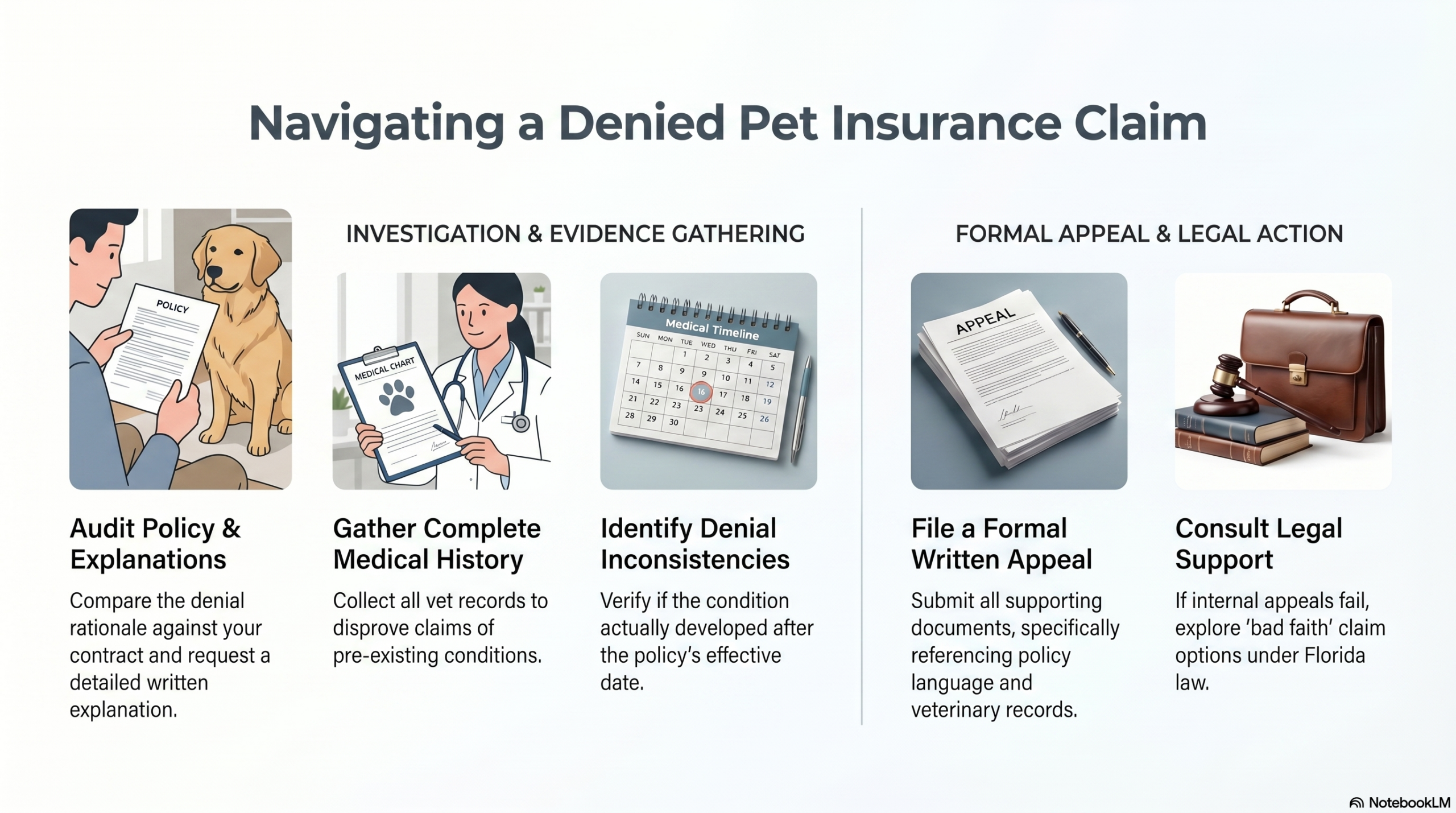

- Review your policy document in full: look for any inconsistency between the denial’s stated rationale and the actual language in your contract.

- Request a written explanation: ask the insurer to provide a detailed written account of why your claim was rejected, citing the specific policy provisions they’re relying on.

- Gather your pet’s complete medical history: full records from every vet your pet has seen. If the insurer is claiming a condition was pre-existing, your records may show otherwise, or may demonstrate that symptoms were never formally diagnosed before.

- Look for inconsistencies in the denial: denials based on pre-existing conditions are frequently overturned when documentation shows the condition developed after the policy effective date.

- File a formal written appeal: with all supporting documents attached. Be specific about why the denial is incorrect, referencing policy language and vet records directly.

- Consult legal support: if the internal appeal doesn’t resolve the issue, you may have grounds for a bad faith pet insurance claim under Florida law.

So, Is Pet Insurance Worth It?

For a young, healthy pet with low near-term risk, you may build more financial security through a dedicated savings account. For an aging pet with known vulnerabilities, or a household where a large vet bill would be destabilizing, a solid plan from a reputable insurer can be really fruitful.

Florida’s recent regulatory changes (mandatory disclosure of exclusions and waiting periods, a 30-day review window with full refunds if no claim is filed) make this a better environment for pet owners than it was just a few years ago.

That said, the value of coverage lawyers in Florida has grown precisely because knowing your rights and actually enforcing them are two different things.

What It All Comes Down To

If you’ve already run into a denial, don’t assume it’s final, and don’t hesitate to bring in professional support if the insurer won’t budge. Your pet’s care is always worth fighting for.

Talk to a Florida pet insurance lawyer today and find out whether your denied claim has grounds for appeal.