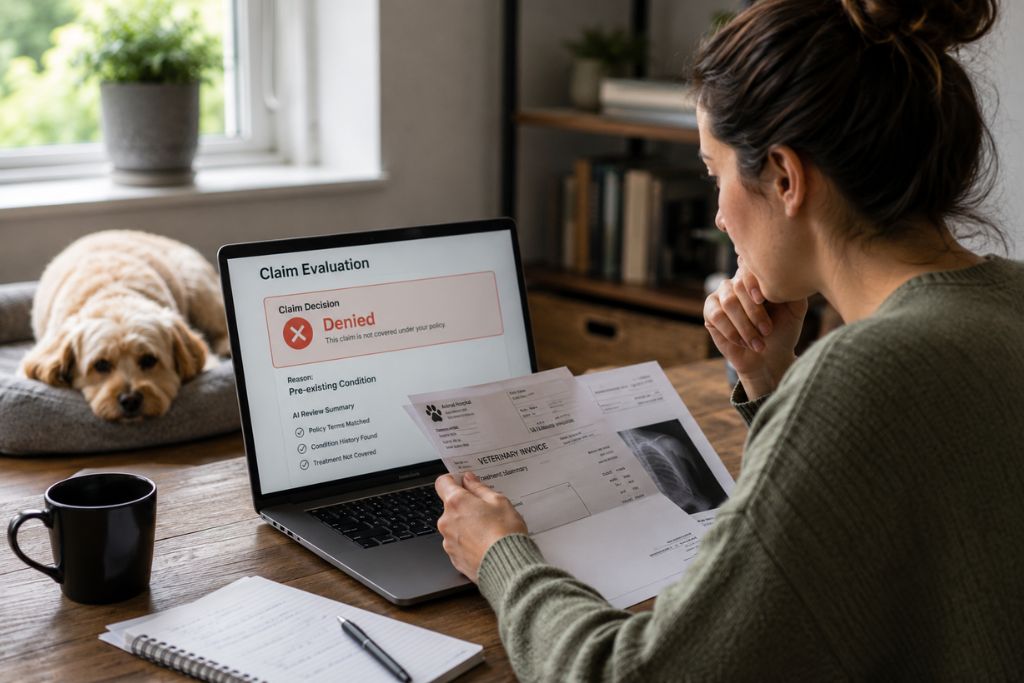

Payments that once felt predictable are now being scrutinized, recalculated, and in many cases reduced through set ups that were never explained at the time of enrollment. Now there’s a growing number of claims that are technically “paid,” but paid far below what owners believed their coverage guaranteed.

HB 655 changes the ground rules around how pet insurance reimbursements must be disclosed and applied. These changes really affect how pet owners plan care, evaluate coverage, and respond when a reimbursement falls short.

Understanding what is changing is essential for anyone trying to protect both their pet’s care and their financial expectations. Let’s begin.

How Pet Insurance Reimbursement really works

Insurance payout for veterinary care tends to be marketed as a simple percentage, but the actual process begins with a misunderstanding of what that percentage is applied to and how insurers determine the reimbursable amount. This typically follows a multi-step calculation:

- The company determines which services are eligible under the policy

- Internal pricing limits or reference amounts are applied

- Only after those reductions does the reimbursement percentage come into play

For pets requiring emergency interventions or specialist care, these reductions are magnified. The gap between the invoice and the reimbursement grows, leading many owners to suspect an error when the issue is actually rooted in how reimbursement is structured.

Benefit Schedules and Fee Limitations Explained

Most reduced compensations for pet medical bills can be traced back to two tools: benefit schedules and fee limitations. These are usually embedded in policy documents, but their practical effect is rarely clear until a claim has already been reviewed and paid.

Benefit schedules operate by assigning a fixed maximum payout to specific treatments, diagnostics, or procedures. Once that ceiling is set, reimbursement cannot exceed it, regardless of the actual cost of care.

Even when veterinary services are medically necessary and priced in line with current legal standards in Florida, the insurer may still limit payment to the scheduled amount.

When applied, they lower the amount the insurer considers eligible for reimbursement before any percentage is calculated. These mechanisms tend to reduce payments in predictable ways:

- A single treatment or diagnostic service may be reimbursed at a rate well below the actual charge.

- Multiple services performed during the same visit may each be subject to separate caps or limits.

- Emergency treatment is often affected most due to higher costs.

HB 655 addresses this by emphasizing the need for clear disclosure and consistent application of benefit schedules and fee limitations, so pet owners are not left discovering these restrictions only when it’s just too late.

What HB 655 Requires Insurers to Disclose

Under the HB 655 payout rules, the provider is expected to make key information available and understandable before a claim is ever filed. Disclosure is intended to give insured pet owners a clear picture of how reimbursement will actually work once care is provided:

- How reimbursement amounts are calculated, including the steps used to determine the payable portion of a claim.

- Whether benefit schedules apply, and which treatments or services are subject to scheduled limits.

- How fee limitations operate, including any internal pricing benchmarks used to reduce payments.

- How advertised reimbursement percentages are applied, and how they interact with caps, schedules, or limits.

These disclosures must be accessible and presented in a way that allows pet families to actually review them without specialized knowledge. Simply referencing limitations in fine print or technical sections of a policy is not sufficient to meet the intent of HB 655.

When an Underpaid Pet Insurance Claim can be challenged

A low reimbursement is not automatically improper, but it should never be accepted at face value without review. Once the calculation behind the payment is examined, the idea is to examine whether the insurer followed the rules it disclosed and whether they were applied consistently with Florida requirements.

The starting point is the method used to arrive at it. When the payment outcome does not align with the policy’s stated terms, further review is often justified:

- Benefit schedules applied without clear prior disclosure.

- Fee limitations that conflict with the policy language, or are applied more broadly than described.

- Reimbursement formulas with higher percentages that are highlighted without explaining reductions.

- Payment reductions applied without a clear calculation breakdown.

When the figures do not reconcile with the policy terms and the insurer’s explanation lacks clarity or supporting detail, an underpaid pet insurance claim may be legally questionable under HB 655.

Why Underpaid Reimbursements Matter for Pet Care

Underpaid reimbursements shape how pet owners approach future care decisions.

After receiving a low payment, owners may hesitate to approve diagnostics, postpone follow-up visits, or decline referrals due to uncertainty about coverage.

So, conditions that are manageable with early intervention may worsen when care is deferred. The state’s emphasis on transparency reflects an understanding that insurance practices influence actual medical decisions. HB 655’s goal is to ensure that owners can make those choices with factual information.

How a Pet Insurance Attorney can help with Underpaid Claims

Resolving an underpaid reimbursement requires isolating where the payment was reduced, how it was justified, and whether that justification aligns with both what the policy disclosed and what the law allows. That is the role Your Pet Attorneys play in these cases.

Our work is built around:

- Policy reconstruction: where benefit schedules, caps, or fee limitations are actually embedded.

- Payment breakdown analysis: how the approved amount was set before the reimbursement percentage was applied.

- Disclosure comparison: reduction mechanisms used in the payment match what was presented at enrollment or in policy materials.

- Communicating discrepancies using documentation and calculation-based arguments rather than general objections.

The Gross Group brings extensive experience in insurance disputes in Florida to the world of pet care. For pet owners who already received a payment but suspect it does not reflect the coverage they purchased, contact immediately.