Cat GI issues (Cat Gastrointestinal Issues) are one of the most prevalent reasons for seeking professional medical care.

You likely prioritize your animal’s health and maintain a policy to mitigate high clinical costs, naturally expecting that the coverage company will act accordingly. However, if the policy issuer labels these digestive episodes as pre-existing conditions, they are effectively barring you from the financial support you anticipated.

And, not every stomach ailment or bout of vomiting qualifies as a permanent exclusion under your contract.

Understanding the line between a chronic exclusion and a reimbursable event is the key to protecting your finances and your cat’s health. So, keep on reading to discover how to ensure you receive the coverage you were promised.

A Common Scenario: When a Digestive Emergency Turns Into a Coverage Dispute

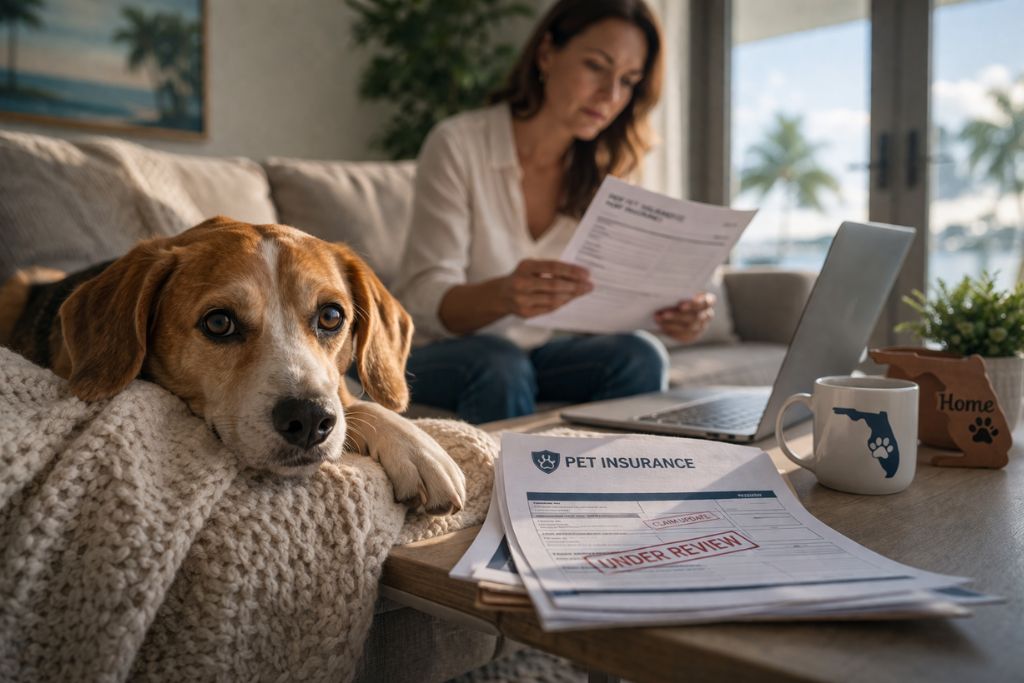

Consider the situation of Luna, the cat.

After a series of diagnostic tests reveal significant internal inflammation, the total medical bill reaches $3,800, leading her owner, Maria, to expect an 80% reimbursement based on her policy terms. Instead, the provider issues a much smaller amount citing a brief note in a three-year-old medical record regarding a “sensitive stomach”.

- A single mention of soft stool recorded years prior serving as the primary legal basis for denying a reimbursement.

- One-time dietary indiscretions: past fluke events that insurers transform into evidence of a continuous, chronic medical condition.

- Long asymptomatic periods: extended stretches of wellness that are often ignored during the insurer’s claim validation process.

For most owners, it seems incomprehensible that a brief medical note from years ago can invalidate support during a current emergency. This tactic of grouping isolated symptoms under the umbrella of “pre-existing” ignores the episodic and curable nature of many gastric issues.

What Counts as Cat Gastrointestinal Issues in Pet Insurance?

Symptoms such as vomiting and diarrhea are frequently the first signs, often leading to pancreatitis or a dangerous intestinal blockage. Also, chronic conditions like inflammatory bowel disease require long-term management and consistent medical intervention.

Because these are some of the most common pet illnesses, they are heavily monitored.

The specific way your pet’s condition is classified, whether as an acute, one-time event or a recurring problem, truly impacts the reimbursement you receive. Also, the insurer might attempt to group a routine diarrhea with a previous unrelated incident, but the medical reality of the condition often tells a different story.

Common Cat GI Issues vs. Pre-Existing Conditions

The insurance provider carries a specific legal obligation to demonstrate with clear evidence that a condition showed clinical signs before the policy’s effective date. You should recognize that a vague veterinary note does not constitute a formal medical diagnosis, and it cannot be used as definitive proof of a prior condition, so:

- Examine your pet’s medical records for precise terminology because insurers often rely on ambiguous notes.

- The burden of legal proof rests entirely with the provider, who must show that the current ailment is identical to a previously treated issue.

- You’ll often succeed when you can prove your pet remained symptom-free for a significant, continuous period.

- Detailed documentation of every veterinary visit ensures that speculative comments by staff do not jeopardize your future claims or lead to unfair exclusions.

You should actively contest any denial that lacks a direct, evidence-based link between past clinical signs and current symptoms to ensure your coverage remains robust and reliable.

Why Digestive Claims in Cats Are Often Scrutinized

This remains a vital component of insurance claims process because gastrointestinal problems occur frequently and incur high costs rapidly; therefore, preparing for an intense investigation into the necessity of ultrasounds or specialized blood work is a fundamental part of managing your policy, so:

- Advocate for full benefits by providing exhaustive documentation that clearly justifies the medical necessity of every diagnostic test performed.

- Reviewing the specific definitions of chronic conditions within your contract helps you challenge instances where a provider attempts to categorize a new illness as an old problem.

- The exact onset of symptoms ensures that they cannot unfairly apply waiting period exclusions to post-effective date health events.

You should remain vigilant against the misapplication of “usual and customary” limits, as these often fail to reflect the actual market costs of modern veterinary diagnostics.

When a Cat Gastrointestinal Claim Denial May Be Questionable

A past episode of food poisoning should not be legally linked to a current diagnosis of kidney issues to justify a pre-existing condition exclusion.

If the policy language remains inconsistent or the insurer failed to provide sufficient disclosure regarding specific medical definitions, you may have legitimate grounds to dispute the decision. Every case depends on:

Any denial that lacks a confirmed medical diagnosis because speculative veterinary notes are insufficient

The insurer’s logic when they attempt to connect unrelated symptoms

Reviewing your policy’s disclosure section to confirm that the definition of a pre-existing condition was clearly communicated before the effective date

Misapplication of waiting periods by providing date-stamped medical records that verify the first appearance of clinical signs

You should always demand a secondary review if the initial assessment fails to incorporate all relevant medical facts to avoid compensation

How Your Pet Attorneys Reviews Cat Gastrointestinal Claim Disputes

For these cases, Your Pet Attorneys conduct a thorough review of all veterinary records and the team evaluates whether the classification of your pet’s illness as pre-existing was medically and legally correct.

The way your pet’s medical history is classified matters significantly for your financial future, so be careful to:

- Consult a pet attorney in Florida to understand how local insurance regulations and state-specific consumer protections apply to your case.

- Florida insurance lawyers specialize in these types of denials to ensure policyholders receive fair treatment under the specific statutes governing the region.

Was your cat’s digestive claim denied? Request a free pet insurance review.