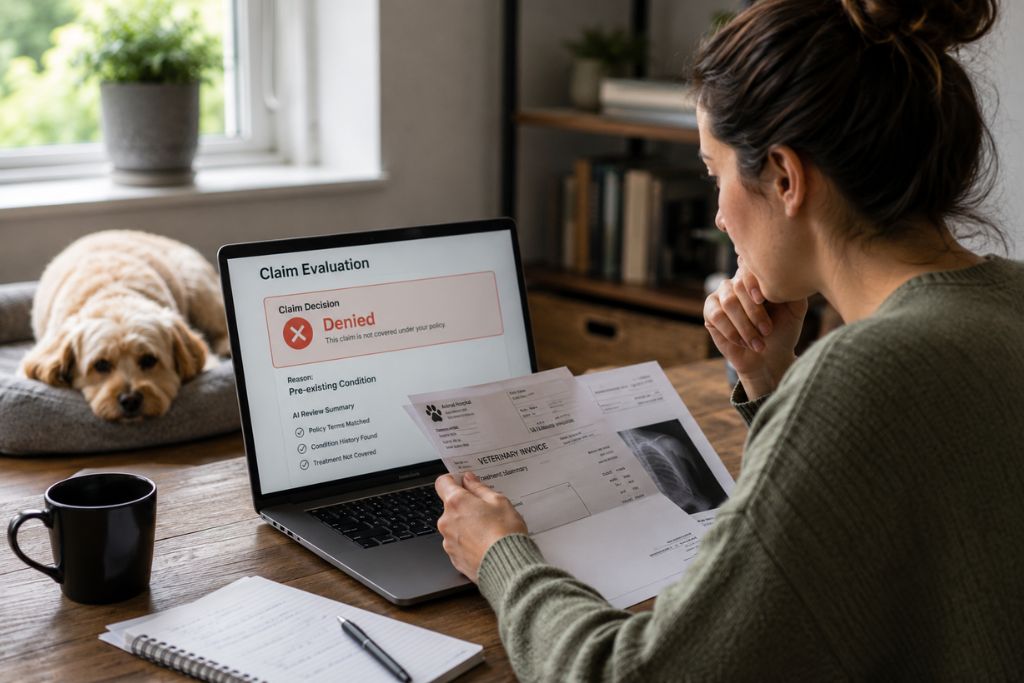

There are few moments that feel as destabilizing as opening a denial letter after doing everything you really believed was right for your pet. Especially trusting that your insurance policy would respond when it mattered most.

This kind of uncertainty forces you to second-guess past decisions.

At this stage, a pet insurance attorney serves as a practical guide through confusing policy language and denial logic. The idea is to help you understand the insurer’s interpretation, and how to regain a sense of direction before accepting a decision with long-term consequences. Let’s dive right in.

How pet insurance claims work

The process usually unfolds in stages that are not always visible to you as a policyholder.

Each step introduces criteria that go beyond medical necessity and focus instead on documentation and policy alignment:

- Veterinary evaluation and treatment, with a diagnosis and treatment based solely on clinical judgment and urgency

- Out-of-pocket payment, since most pet insurance policies require you to pay the full cost upfront

- Claim submission: sending invoices, medical records, and timelines that may already contain notes

- Policy definitions, exclusions, benefit limits, and waiting periods are applied to the file

- Reimbursement decision, often with brief explanations that reference policy sections rather than medical reasoning

Because this system evaluates coverage after treatment has already occurred, many pet owners only discover how their policy is interpreted once a contested pet insurance claim is denied.

This tends to explain why understanding this can prevent unrealistic expectations and support more informed decisions later.

What is a pre-existing condition in pet insurance?

They’re tied to earlier symptoms, clinical notes, or observations that appear in your pet’s medical history, even if no treatment was required at the time.

Insurance companies can apply this concept using internal interpretations that are rarely explained clearly, which is why reviewing these definitions with a pet insurance attorney can help you understand whether the exclusion was applied fairly or stretched beyond its original intent. Common elements:

- Waiting periods: separating conditions that appear before coverage becomes active

- Symptom-based evaluations: vomiting, limping, or weight loss noted in past visits are later connected to unrelated diagnoses

- Broad exclusion language being used to group multiple conditions under a single category

- Reviewing records backward once a serious diagnosis appears

Many denials are driven less by clear medical conclusions and more by how insurers interpret fragments of your pet’s history after the fact. A lawyer can help you decide whether an exclusion was applied reasonably or expanded beyond what your policy actually allows.

Why pet insurance claims are denied based on pre-existing conditions

The denial process often follows a very predictable pattern that prioritizes contractual flexibility over medical nuance, which is why so many pet owners feel as blindsided by the outcome as it comes.

Insurance companies assemble a narrative from past veterinary notes, isolated symptoms, and broad policy definitions that allow them to link unrelated events across time.

A brief mention of vomiting or limping in an old record can later be used to block coverage for a much more serious condition. This approach shifts the focus away from when a condition was actually identifiable and toward how medical history can be interpreted retroactively.

How pet insurance attorneys challenge pre-existing condition denials

It involves a methodical review that goes far beyond questioning the insurer’s conclusion, because these decisions are built on how policy language is applied to medical history. The medical seriousness of the condition itself tends to fade here.

Here, a Florida insurance attorney really shines by:

- A line-by-line reading of the policy and each section is examined on its own to understand how coverage, exclusions, and conditions interact

- Particular attention to how exclusions are defined, how waiting periods are calculated, and how flexible or open-ended terms are meant to operate together

- Identifying whether the same definitions were applied throughout the pet insurance coverage claim or adjusted selectively at different stages to justify the denial

Veterinary records are examined in strict chronological order, separating isolated or nonspecific symptoms from documented patterns that could reasonably indicate an ongoing condition. The idea here is to challenge any attempt to link past notes to a diagnosis that could not have been medically identified at that time.

The attorney also evaluates how the insurer framed its narrative.

Pinpointing assumptions, gaps, or selective use of records, and restructures the appeal around evidence and internal consistency, shifting the focus to whether the denial was supported by fair interpretation rather than by hindsight or cost-driven reasoning.

Final thoughts: understanding your policy before accepting a denial

Once you understand how pet insurance claims work, you see why so many disputes start after treatment is already completed.

Pre-existing conditions sit at the center of this problem because insurers frequently use broad exclusions to widen the scope of what they can deny. That is why experienced guidance matters early.

A pet insurance lawyer can evaluate the policy and the records as they actually unfolded, identify a bad narrative that can be challenged before the consequences become permanent.

A claim has been denied and the insurer’s explanation leaves you questioning how your policy was applied? Take a moment to seek clarity through a case review and reach out to The Gross Group.