With HB 655 set to take effect on January 1, 2026, Florida aims to redefine the legal standards that insurers must meet when considering preexisting conditions for pets.

Most pet owners don’t realize how much of their pet’s future care is quietly determined by whether treatment will be reimbursed or denied. In 2026, these hidden factors will matter more than ever.

HB 655 shifts obligations onto insurers and changes how denials should be justified. Yet many policyholders still remain unaware of how these rules affect medical decisions for their pets.

Understanding this new law is essential to consider whether a legal review is actually warranted. Let’s break it down.

What Is a Preexisting Condition Under HB 655?

Under Florida’s new basis, a preexisting condition is defined by what can be objectively shown in the pet’s medical record at specific points in time. It may be classified as such only if it involves at least one:

- Treatment for the condition

- A formal diagnosis of the condition

- Documented clinical signs or symptoms that are medically connected to the condition later claimed

This limits retroactive reasoning. An insurer cannot simply look at a later diagnosis and work backward unless the earlier records clearly support that connection. The focus is on what became clear later.

Equally important, 2025 Florida Statutes for HB 655 addresses renewals, as once a condition is covered under an active policy, it cannot later be reclassified as preexisting simply because the policy renews.

Continuous coverage preserves status, always.

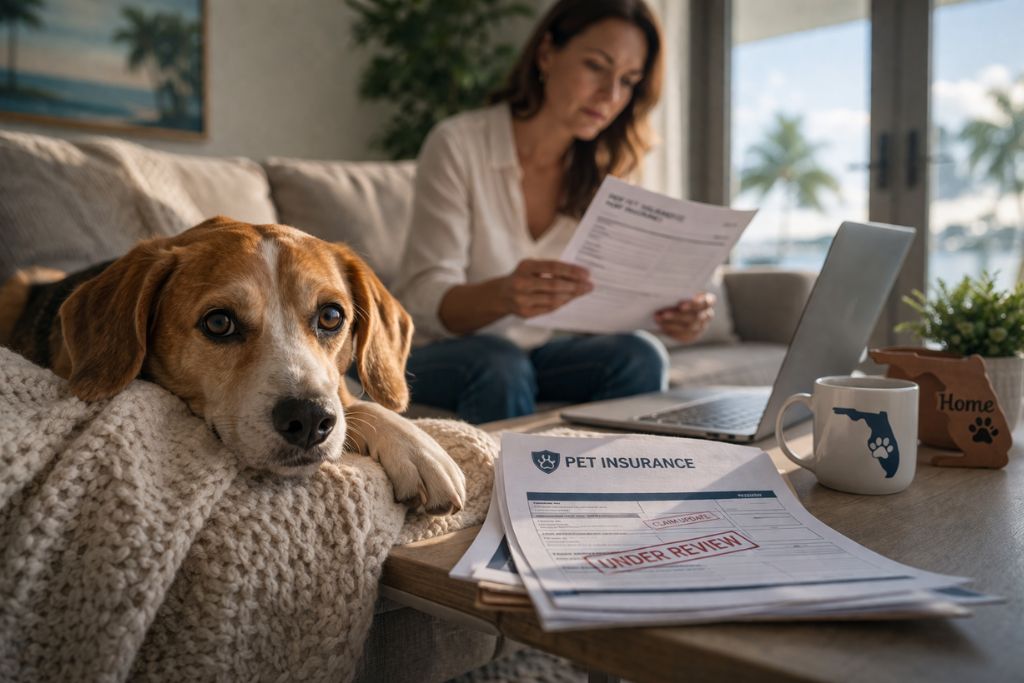

Why Pet Insurance Companies Commonly Deny Claims as Preexisting

We talk about one of the most effective tools insurers have to control risk and limit claim payouts while remaining within contractual boundaries. Several recurring practices explain why:

- Expansive interpretation of nonspecific symptoms: mild or temporary symptoms may later be framed as early evidence of a serious condition that was not suspected at the time.

- Selective reliance on veterinary records while ignoring the broader context of the visit.

- Minimal explanation in denial communications: referencing “medical history” without identifying the specific definition used to justify the exclusion.

HB 655 changes the tolerance for ambiguity and insurers are expected to explain how and why a condition meets the legal definition, not merely state that it does.

The Burden of Proof: What Insurers Must Show Under HB 655

Mainly, the allocation of responsibility. When an insurer denies a claim based on a preexisting condition, the burden of proof rests only with the insurer. For this, three things must align:

- The insurer must identify specific medical records it relies upon.

- The records must demonstrate that the condition existed before coverage or during the waiting period.

- An explanation must connect those records to the policy’s written definition of a preexisting condition.

If the insurer cannot substantiate the exclusion with verifiable documentation, the denial may be subject to challenge. Generic references without a clear evidentiary link fall short of what the law requires.

For those who want to review the law at its source, the Florida House’s bill offers the most direct and reliable overview of HB 655.

Common Disputes Involving Preexisting Conditions

Vague symptoms later used as definitive proof

Your dog may have been seen months before coverage began for occasional stiffness or fatigue, with no diagnosis made at the time. After coverage is in place, the dog is later diagnosed with a joint disorder and the insurer may then argue that those earlier signs show the condition existed all along.

Disputes like this usually hinge on whether the initial symptoms can be medically connected to the later diagnosis or whether that connection is merely based on speculation rather than documented evidence.

Unrelated medical issues grouped together

Your cat is treated for skin irritation and later develops an endocrine disorder. The coverage provider may attempt to classify both under a single preexisting umbrella, even when veterinary medicine does not support that linkage. Now, the dispute centers on medical relevance rather than chronology alone.

Chronic conditions mischaracterized across time

Not every illness appears all at once and some take shape slowly, revealing themselves over time rather than in a single visit.

The insurance company may point to nonspecific observations and treat them as proof that a chronic condition was already underway, even when the veterinarian had no reason to suspect it before. Now the focus is on whether the denial is grounded on conclusions drawn only after the diagnosis became clear.

When a Pet Insurance Attorney Can Challenge a Preexisting Condition Denial

Legal support becomes relevant when a denial rests on weak or unclear evidence.

If the insurer does not point to specific medical records or relies on generalized references to a pet’s history, the basis for the decision may be questionable. This is especially true when earlier veterinary notes are used out of context to support a conclusion that was never made at the time of treatment.

A Florida pet insurance attorney focuses on whether the insurer followed the policy terms and met its obligations under HB 655, evaluating the denial solely on documentation and compliance.

How The Gross Group Your Pet Attorneys Helps Pet Owners Fight Preexisting Condition Denials

The Gross Group is a firm that knows how to fight for the benefits the policyholder is entitled to. The work focuses on:

- Coverage language is reviewed line by line to confirm whether exclusions were applied as written and whether the insurer followed the disclosure requirements tied to Florida’s New Pet Insurance Law (HB 655).

- Dates, symptoms, notes, and diagnoses are placed in context to see what was actually known at the time and what was determined later.

- The denial is measured against the insurer’s obligation to prove a preexisting condition with clear and specific evidence.

- If that proof is missing, incomplete, or based on assumptions rather than records, the issue is identified and documented.

- Insurers are addressed directly, with responses grounded in policy language and medical documentation rather than emotion or speculation.

The Gross Group, drawing on broader experience in Florida insurance disputes to inform how exclusions are interpreted and challenged. Get in touch to get high-value legal guidance.